In 2025, mastering personal finance and budgeting is a game-changer for Americans facing economic uncertainty. With consumer confidence at a record low, as recent surveys show, taking control of your finances through personal finance and budgeting can help you thrive. For instance, 66% of U.S. GDP relies on consumer spending, yet many struggle with rising costs and debt. Whether you’re saving for a house, paying off credit cards, or planning for retirement, this guide offers practical steps to succeed. Let’s dive into personal finance and budgeting strategies to make 2025 your year of financial freedom!

If you’re just starting, check out my previous post on essential money-saving tips for beginners to build a strong foundation for personal finance and budgeting.

Why Focus on Personal Finance and Budgeting Now?

First, let’s understand why personal finance and budgeting are so crucial in 2025. Inflation and high interest rates are squeezing budgets, making it harder to save. However, a solid plan can help you manage money effectively. For example, budgeting aligns your spending with your goals, whether that’s traveling, starting a family, or retiring early. Additionally, personal finance and budgeting reduce financial stress by giving you control. So, let’s explore how to create a plan that works for you.

How to Create a Budget for 2025

A budget is the foundation of personal finance and budgeting. Essentially, it’s a roadmap for your money, showing where it goes and how to reach your goals. Here are three methods to try:

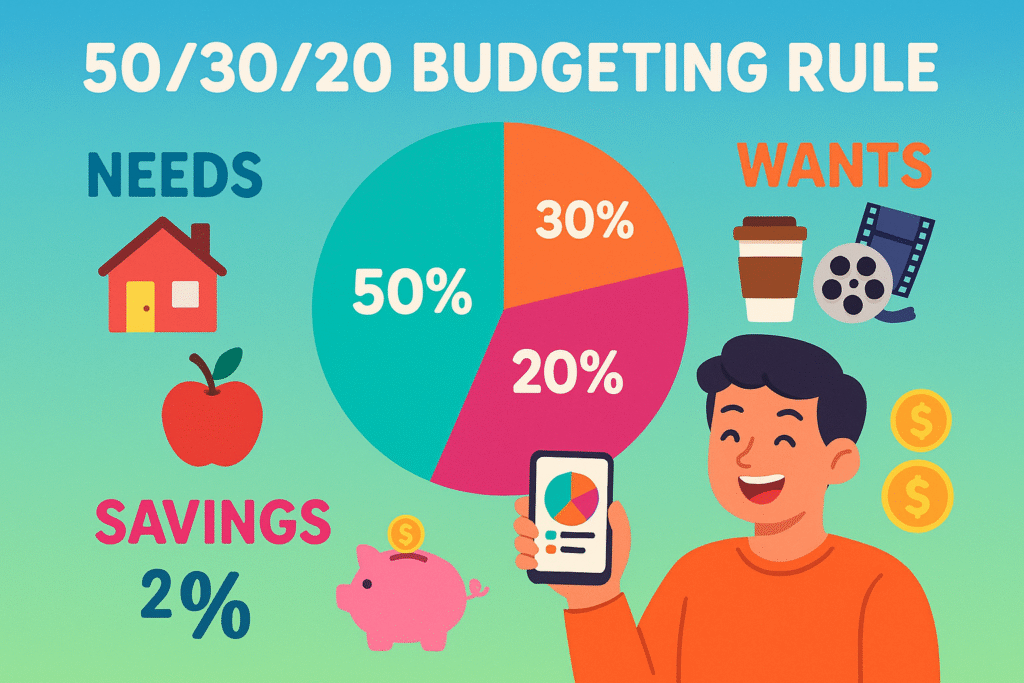

- 50/30/20 Rule: Allocate 50% of your income to needs (e.g., rent, groceries), 30% to wants (e.g., entertainment), and 20% to savings or debt repayment. This method is beginner-friendly and flexible.

- Zero-Based Budgeting: Give every dollar a purpose, ensuring your income minus expenses equals zero. Tools like YNAB can help you track this method effectively.

- Envelope System: Use cash for specific categories and stop spending when the envelope is empty. This helps curb overspending.

Pro Tip: Apps like Simplifi or Quicken Classic make budgeting easier. For instance, Simplifi offers a user-friendly interface, while Quicken provides detailed account management.

Strategies to Tackle Debt Effectively

Next, let’s tackle debt—a major hurdle in personal finance and budgeting. In 2025, high interest rates will make debt management critical. For example, U.S. credit card debt reached $1.14 trillion in 2024, showing how widespread this issue is. Here’s how to address it:

- Debt Snowball: Pay off smaller debts first for quick wins. For example, clear a $500 credit card before a $10,000 student loan.

- Debt Avalanche: Focus on high-interest debts to save money over time. For instance, prioritize a 20% APR credit card over a 4% car loan.

- Consolidation: Combine debts into one loan with a lower rate. Platforms like SoFi offer great options.

Moreover, apps like YNAB can track your debt payments, keeping you on track with your personal finance and budgeting goals.

Building an Emergency Fund in 2025

Another key step in personal finance and budgeting is building an emergency fund. This safety net covers 3-6 months of expenses, protecting you from unexpected costs. In 2025, with economic uncertainty, this is essential.

Start small: Save $500, then $1,000, and keep going. For example, automate transfers to a high-yield savings account with banks like Ally or Marcus, which offer 4% APY. A $5,000 fund at 4% earns $200 annually—free money to secure your future. This step strengthens your personal finances and budgeting plan significantly.

Investing for Long-Term Wealth Growth

Beyond saving, personal finance and budgeting include growing your money through investing. In 2025, investing is more accessible than ever. Here’s how to start:

- Retirement Accounts: Contribute to a 401(k) or IRA. If your employer matches contributions, take full advantage—it’s free money!

- Index Funds: Invest in low-cost ETFs like the S&P 500 for steady growth. Platforms like Vanguard or Fidelity simplify this process.

- Robo-Advisors: Use apps like Betterment for automated investing tailored to your goals.

Interestingly, 60% of Americans are investing, but many hesitate due to fear. Start small, even $50 a month, and watch your wealth grow through personal finance and budgeting.

Embrace Frugal Living for Savings

Frugal living is a powerful part of personal finance and budgeting. In 2025, with inflation still a concern, spending smarter can save you hundreds. Here are some tips:

- Cut Subscriptions: Review streaming or app subscriptions and cancel unused ones.

- Meal Planning: Save $100+ monthly by cooking at home. Check out Budget Bytes for affordable recipes.

- Negotiate Bills: Call your internet provider to lower rates—it often works!

Stay Educated and Motivated in Your Journey

Finally, staying educated is vital for personal finance and budgeting success. In 2025, resources are abundant to keep you learning:

- Books: Read The Millionaire Next Door for timeless wealth-building tips.

- Podcasts: Listen to ChooseFI for practical advice on personal finance and budgeting.

- YouTube: Follow The Financial Diet for relatable money tips.

Additionally, join communities like Reddit’s r/personalfinance for support. Celebrate small wins, like paying off a credit card, to stay motivated in your personal finance and budgeting journey.

Take Control with Personal Finance and Budgeting

In conclusion, personal finance and budgeting in 2025 are about empowerment. Despite economic challenges, you can build a secure future by budgeting wisely, tackling debt, saving diligently, and investing strategically. For more tips, explore my post on smart saving hacks for 2025. Start today—download a budgeting app, cut one expense, or open a savings account. Every step counts!

Share your favorite budgeting tip in the comments, and let’s inspire each other to make 2025 a year of financial success through personal finance and budgeting!

Disclaimer: The information provided in this blog post is for educational purposes only and does not constitute financial advice. Always consult with a qualified financial advisor before making any financial decisions. The author and website are not responsible for any financial outcomes resulting from the use of this information.