Introduction: Social Security Benefits Face a Transformative 2025

You’re checking your bank account, expecting a slight bump in your social security benefits thanks to the 2025 cost-of-living adjustment (COLA), but instead, you notice a deduction—Medicare premiums have eaten into your raise! As of April 28, 2025, the Social Security Administration (SSA) has rolled out a 2.5% COLA, tech upgrades like secure digital SSN access, and policy shifts that could reshape how millions access benefits. Having followed these changes closely, I’ve seen firsthand how they can catch beneficiaries off guard—my neighbor, a retiree, was stunned by the new in-person identity proofing rules. Let’s break down these updates, compare their impacts, uncover key insights, and see what they mean for you.

Comparing Social Security Benefits: 2024 vs. 2025 Updates

The landscape of social security benefits has shifted significantly from 2024 to 2025. Let’s compare the key changes to understand their impact on beneficiaries and workers.

COLA Adjustments and Benefit Increases

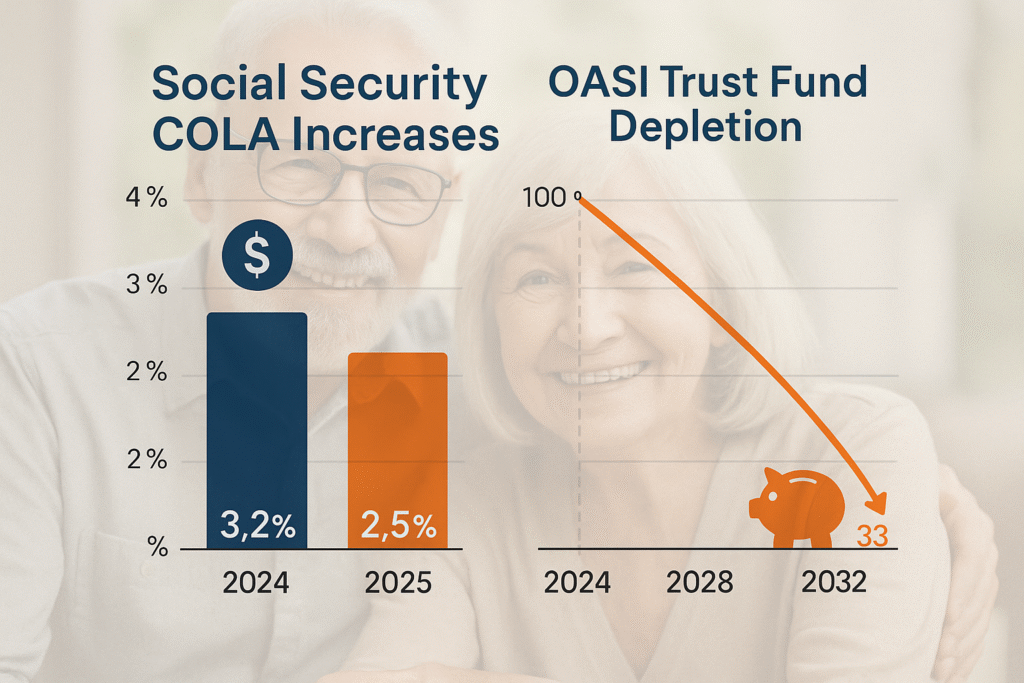

- 2024 COLA: A 3.2% increase, adding about $59 to the average retiree’s monthly check, bringing it to $1,927.

- 2025 COLA: A smaller 2.5% increase, boosting the average retiree’s benefit by $49 to $1,976. Couples see a $75 rise to $3,089.

- Impact: The 2025 COLA, the lowest since 2020, reflects cooling inflation but doesn’t ease the burden of already high prices for essentials like groceries and housing.

Earnings Limits and Taxable Wages

| Category | 2024 | 2025 |

|---|---|---|

| Earnings Limit (Under FRA) | $22,320 | $23,400 |

| Earnings Limit (At FRA) | $59,520 | $62,160 |

| Maximum Taxable Earnings | $168,600 | $176,100 |

- Earnings Limits: If you’re under full retirement age (FRA), the SSA deducts $1 for every $2 earned over $23,400 in 2025, up from $22,320 in 2024. At FRA, the limit rises to $62,160 from $59,520, with $1 deducted for every $3 over.

- Taxable Wages: The maximum earnings subject to Social Security tax increased to $176,100, meaning higher earners pay more into the system at the 6.2% rate.

Policy and Tech Changes

- 2024: The SSA focused on post-pandemic recovery, encouraging online services but still allowing drop-in office visits.

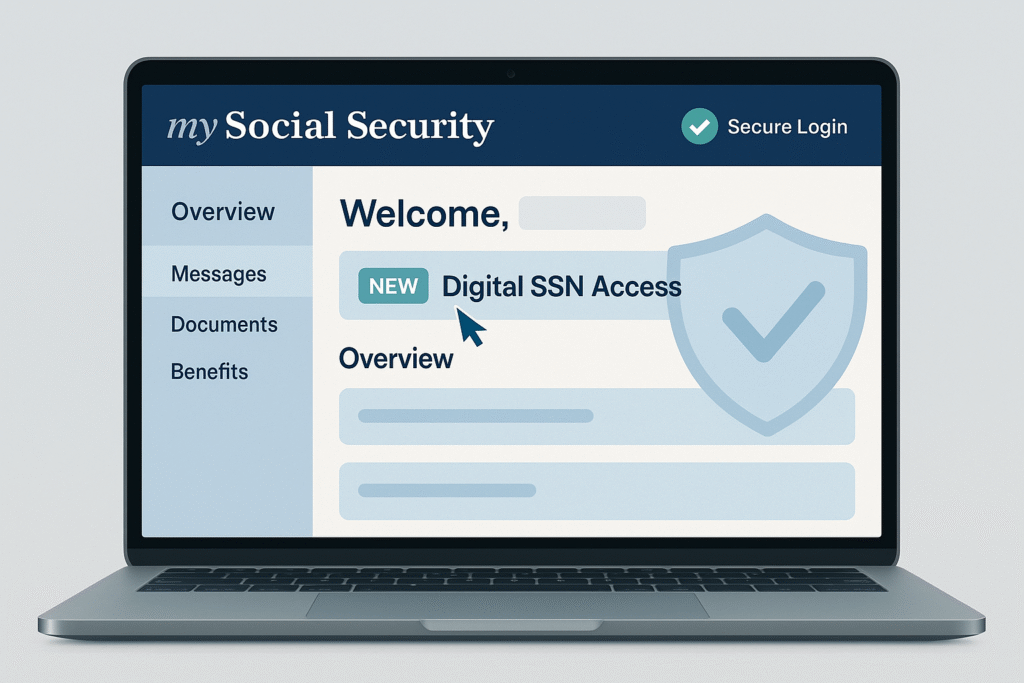

- 2025: Major shifts include mandatory in-person identity proofing for certain claims starting April 14, enhanced telephone fraud prevention, and secure digital SSN access via my Social Security accounts.

These changes aim to modernize services but have sparked concerns about accessibility, especially for older adults and those with disabilities.

Key Insights: What’s Shaping Social Security Benefits in 2025?

Let’s dive into the forces driving these updates to social security benefits, blending recent developments, expert perspectives, and my own observations.

Tech Upgrades: A Double-Edged Sword

The SSA has introduced several tech-focused improvements in 2025:

- Digital SSN Access: As of April 25, beneficiaries can securely access their Social Security number online via my Social Security accounts, reducing reliance on physical cards.

- Telephone Fraud Prevention: Starting April 14, new anti-fraud tools analyze patterns in telephone claims, requiring in-person identity proofing if suspicious activity is detected.

- System Migration Concerns: Experts like Jason Fichtner, a former SSA deputy commissioner, warn that the agency’s plan to transition from COBOL coding in mere months risks disrupting benefit payments—a process that typically takes years.

I’ve seen mixed reactions to these changes. My neighbor, a tech-savvy retiree, loves the digital SSN access, but a friend with limited internet struggled with the new in-person proofing rules, driving 45 miles to an SSA office.

Policy Shifts: Fairness and Accessibility Challenges

The Social Security Fairness Act has brought significant relief in 2025:

- WEP and GPO Repeal: Over 3.2 million beneficiaries, including teachers and federal workers, see increased monthly benefits and $14.8 billion in retroactive payments by April.

- Spousal Benefits Update: The option to alternate between personal and spousal benefits for strategic claiming ended for those born after January 2, 1954, simplifying but limiting flexibility.

However, the Trump administration’s changes have raised alarms:

- In-Person Identity Proofing: Starting April 14, claims for retirement or survivor benefits require online or in-person proofing, posing hurdles for those without digital access.

- Office Closures: Reports of 47 local SSA office closures in the South, coupled with a staff reduction to 50,000, could limit access, despite the SSA’s claim that virtual services suffice.

Financial Outlook: A Looming Crisis?

The 2024 SSA Trustees Report projects the Old-Age and Survivors Insurance (OASI) Trust Fund will deplete by 2033, paying only 79% of benefits thereafter. The combined OASDI fund lasts until 2035, covering 83% of benefits. These projections predate 2025’s policy shifts, but experts like Romina Boccia from the Cato Institute argue that administrative changes won’t address this looming shortfall.

I find this disconnect troubling—while the SSA focuses on efficiency, the bigger issue of trust fund depletion feels ignored, leaving future retirees like me uneasy.

Impact of External Factors: Tariffs and Inflation

The 2025 global tariff war, with 145% tariffs on Chinese imports and a potential 400% hike, indirectly affects social security benefits. Rising costs for goods could outpace the 2.5% COLA, and some experts worry tariffs might strain SSA funding if economic growth slows. Meanwhile, Medicare Part B premiums rose to $185 in 2025, reducing net benefits for many—like a reader on the SSA blog who saw their $185 payment drop to $35 after deductions.

Conclusion: What Do These Changes Mean for You?

In 2025, social security benefits are at a crossroads—modernization offers convenience, but accessibility hurdles and a looming trust fund crisis cast shadows. The 2.5% COLA provides some relief, yet external pressures like tariffs and Medicare costs highlight the need for broader reform. My take? Stay proactive—set up a my Social Security account, check your benefit notices, and plan for potential disruptions.

What’s your experience with these changes in social security benefits? Share your thoughts below! For more financial insights, explore our latest posts. Let’s navigate this together—share this post if you found it helpful!